Market Review 2nd August 2024

Simplify the craziness

DAILY REVIEW

N

4 min read

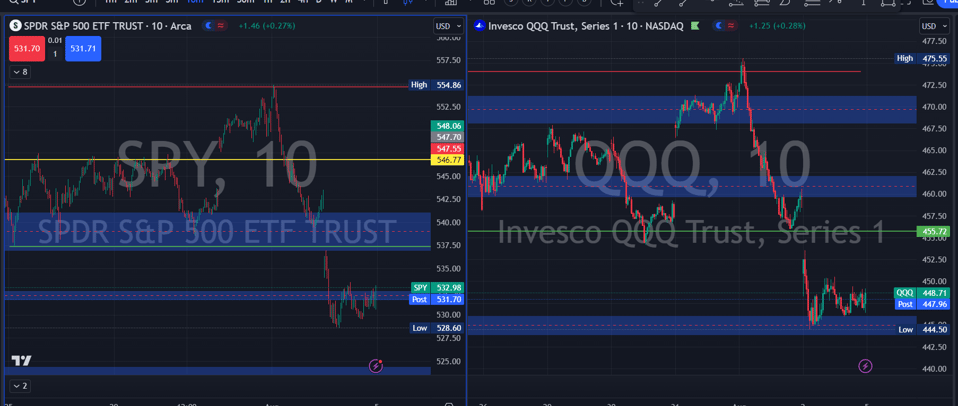

Equity markets experienced a significant downturn on Friday, driven by a disappointing U.S. jobs report that raised concerns about economic growth. The U.S. unemployment rate increased to its highest level since 2021, and nonfarm employment growth fell well below expectations. This article provides a comprehensive analysis of the day's market movements, the implications of the jobs data, and a detailed look at the current earnings season.

U.S. Jobs Data and Market Reaction

Softer-Than-Expected Jobs Report

The U.S. nonfarm payrolls for July increased by only 114,000, significantly missing the consensus forecast of 175,000. This lower-than-expected job growth has heightened fears about the U.S. economic outlook. The unemployment rate rose to 4.3%, the highest since 2021, up from 3.7% at the beginning of the year. This rise in unemployment signals a potential slowdown in the labor market.

In addition to the rise in the unemployment rate, the number of people working part-time for economic reasons increased to 4.6 million. This figure is now in line with pre-pandemic levels, indicating that many workers are unable to find full-time employment due to business conditions. On the wage front, average hourly earnings grew by 3.6% year-over-year, slightly below the expected 3.7% growth. This slower wage growth further adds to concerns about the health of the economy.

Market Performance

The disappointing jobs data triggered a broad sell-off in equity markets. The S&P 500 saw a notable shift towards risk-off sentiment, with consumer staples emerging as the top-performing sector. In contrast, growth and cyclical sectors such as consumer discretionary, technology, and financials suffered sharp declines. The TSX also felt the pressure, declining by over 2%.

Global markets mirrored the negative sentiment in the U.S. Asian markets were particularly hard hit, with Japan's Nikkei plummeting nearly 6%. European markets also sold off amid growing concerns about U.S. economic growth, reflecting a widespread risk aversion among investors.

Bond Market Rally

In response to the soft labor market data, bond markets rallied sharply. The yield on the 10-year Government of Canada (GoC) bond fell by approximately 11 basis points to 3.01%, while the yield on the 10-year U.S. Treasury dropped nearly 20 basis points to around 3.8%. This rally in bond prices indicates that investors are seeking safety in government debt amid increasing economic uncertainty.

Implications of the Jobs Data

Growth Concerns

The weaker-than-expected jobs report has amplified concerns about U.S. economic growth. This sentiment was already on the rise following an increase in initial jobless claims and a soft ISM manufacturing report released earlier. The cumulative effect of these indicators suggests that the U.S. economy may be facing more significant headwinds than previously anticipated.

Futures markets have responded by adjusting their expectations for Federal Reserve actions. There is now a roughly 70% chance of a 50-basis-point interest rate cut at the Fed's September meeting. Additionally, markets are pricing in a total of 125 basis points of rate cuts by the end of the year. These expectations reflect growing concerns that the Fed may need to take more aggressive measures to support economic growth.

Earnings Season in Full Swing

Technology Heavyweights Report

Earnings season remains a focal point for markets, with several technology giants reporting their quarterly results. Apple and Amazon both exceeded earnings expectations when they reported after the bell on Thursday. However, Amazon's cautious forward guidance weighed on its shares, leading to a decline in its stock price. In contrast, Apple managed to finish higher, buoyed by its positive earnings report.

Semiconductor company Intel also reported after the market close on Thursday, but its earnings fell short of expectations. Additionally, Intel announced plans to suspend its dividend, which led to a sharp sell-off in its shares, with the stock closing down by over 25%.

Overall Earnings Performance

Despite recent volatility, the overall earnings performance for the second quarter has been strong. Approximately 75% of companies in the S&P 500 have reported their results, with about 78% of those companies exceeding expectations. This robust performance has led to an upward revision of earnings growth estimates for the quarter, now expected to be around 10%, up from the 8% forecasted at the end of June.

Looking ahead to the full year, earnings are projected to grow by roughly 11%. If achieved, this would represent the strongest growth rate since 2021. For the TSX, less than 50% of companies have reported their second-quarter results. Current estimates suggest earnings growth of 4.6% for the quarter, indicating a more modest performance compared to the S&P 500.Most Actively Traded US Stocks

Name Ticker Percentage Change (Daily)

NVIDIA Corporation NVDA -1.78%

Amazon.com, Inc. AMZN -8.78%

Apple Inc. AAPL +0.69%

Tesla, Inc. TSLA -4.24%

Microsoft Corporation MSFT -2.07%

Meta Platforms, Inc. META -1.93%

Advanced Micro Devices, Inc. AMD -0.03%

Intel Corporation INTC -26.06%

Super Micro Computer, Inc. SMCI -7.08%

Broadcom Inc. AVGO -2.18%

JP Morgan Chase & Co. JPM -4.24%

Micron Technology, Inc. MU -8.68%

Alphabet Inc. GOOG -2.35%

UnitedHealth Group Inc. UNH +2.98%

Bank of America Corporation BAC -4.86%

Goldman Sachs Group, Inc. GS -5.89%

Eli Lilly and Company LLY -3.36%

McDonald's Corporation MCD +2.95%

Booking Holdings Inc. BKNG -9.17%

QUALCOMM Incorporated QCOM -2.86%

Exxon Mobil Corporation XOM -0.06%

Applied Materials, Inc. AMAT -7.38%

Netflix, Inc. NFLX -1.79%

Lam Research Corporation LRCX -8.11%

Coinbase Global, Inc. COIN -3.86%

MicroStrategy Incorporated MSTR -4.22%

List of Tickers

$NVDA $AMZN $AAPL $TSLA $MSFT $META $AMD $INTC $SMCI $AVGO $JPM $MU $GOOG $UNH $BAC $GS $LLY $MCD $BKNG $QCOM $XOM $AMAT $NFLX $LRCX $COIN $MSTR $PG $COST $BA $CVX $CRWD $MRK $V $JNJ $C $MA $WMT $UBER $CRM $KO $DASH $WFC $ADBE $PYPL $DIS $HD

Conclusion

The sharp decline in equity markets on Friday underscores the significant impact of economic data on investor sentiment. The softer-than-expected U.S. jobs report has heightened concerns about the economic outlook, leading to broad-based selling in equities and a rally in bond markets. While the earnings season has provided some positive news, particularly in the technology sector, the overall market environment remains challenging.

Investors will be closely watching upcoming economic data and Federal Reserve actions to gauge the future direction of the markets. The heightened volatility and mixed signals from various sectors suggest that the path forward may be fraught with uncertainty. As always, maintaining a diversified portfolio and staying informed about market developments will be crucial for navigating these turbulent times.