Market Review 26th July 2024

Simplify the craziness

DAILY REVIEW

N

2 min read

Daily Market Summary

Overview

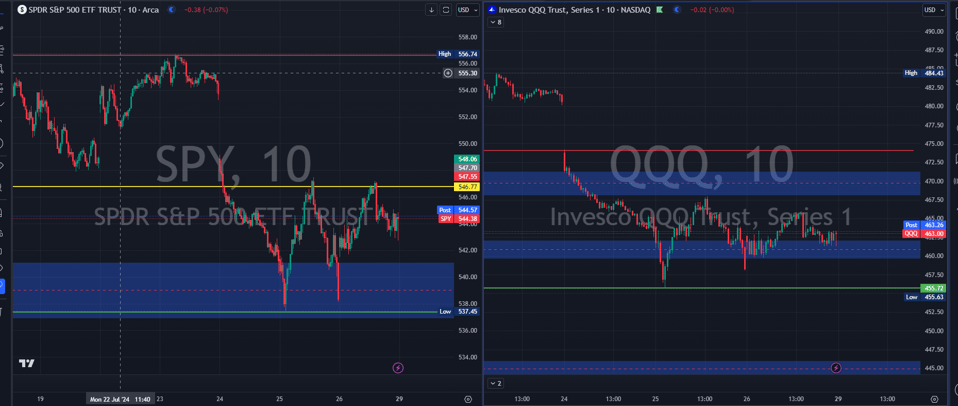

On Friday, the TSX and major U.S. equity indexes closed higher, with small- and mid-cap stocks outperforming large-cap stocks. Industrial and real estate sectors led the gains, while bond yields decreased. The 10-year Government of Canada yield was at 3.32%, and the 10-year U.S. Treasury yield was at about 4.19%. Global markets in Asia and Europe also traded higher, recovering from the previous day's sell-off. The U.S. dollar weakened against major currencies. In commodities, WTI oil prices fell due to concerns over demand from China, while gold prices rose.

Key Inflation Measures

The Fed's preferred inflation measure, the core personal consumption expenditure (PCE) price index, rose 2.6% annualized through June, slightly above estimates but unchanged from the previous month. The headline PCE decreased to 2.5% year-over-year, aligning with expectations. Consumption expenditures increased by 0.3%, slightly lower than May's 0.4%, indicating a resilient yet cautious consumer. Personal income grew by 0.2%, below expectations and the prior month. These inflation readings suggest the Fed might cut interest rates later this year, potentially in September and December, as inflation is expected to moderate further.

Corporate Earnings

With 41% of S&P 500 companies reporting second-quarter earnings, 78% have surpassed analyst estimates, with an average upside surprise of 4.4%. Year-over-year earnings growth for the first quarter is at 9.8%, the highest since Q4 2021. Earnings growth is projected to rise to 10.6% for the year, with eight of the 11 sectors reporting higher earnings year-over-year. The broadening of earnings performance could help lagging sectors catch up to the technology and communications services sectors, which have driven market gains.

Market Movers

Stocks rose sharply after the personal consumption expenditures price index met expectations, reinforcing the belief that the Fed will cut rates in September. The positive response to earnings news and buying in mega-cap and semiconductor stocks also contributed to the market's upward bias. Lower Treasury yields further supported gains.

Closing Summary

Dow Jones: +654.27 at 40,589.14 (+1.6%)

Nasdaq: +176.16 at 17,357.88 (+1.0%)

S&P 500: +59.88 at 5,459.10 (+1.1%)

Russell 2000: +1.7%

Advancers outpaced decliners by a significant margin, with a broad-based advance across all sectors. The industrial and materials sectors led the gains, while the energy sector logged the smallest gain.

Notable Earnings

3M (MMM): +23.0% after beating earnings estimates and raising guidance.

Mohawk (MHK): +19.5% on strong earnings.

Charter Communications (CHTR): +16.6% after reporting better-than-expected earnings.

Norfolk Southern (NSC): +10.9% on solid earnings.

Economic Data

June Personal Income: 0.2% (vs. 0.4% expected)

June Personal Spending: 0.3% (as expected)

June PCE Prices: 0.1% (as expected)

June Core PCE Prices: 0.2% (as expected)

University of Michigan Consumer Sentiment (July): Final 66.4 (as expected)

Big Movers Table

StockMovement (%)Dexcom (DXCM)-40.7%3M (MMM)+23.0%Mohawk (MHK)+19.5%Charter Comm (CHTR)+16.6%Norfolk Southern (NSC)+10.9%Coursera (COUR)+44.7%Deckers Outdoor (DECK)+6.3%Ford Motor (F)+0.3%Alphabet (GOOGL)-0.2%Nvidia (NVDA)+0.7%Biogen (BIIB)-7.2%Bristol Myers (BMY)+11.5%

References