Market Review 25th July 2024

Simplify the craziness

DAILY REVIEW

N

2 min read

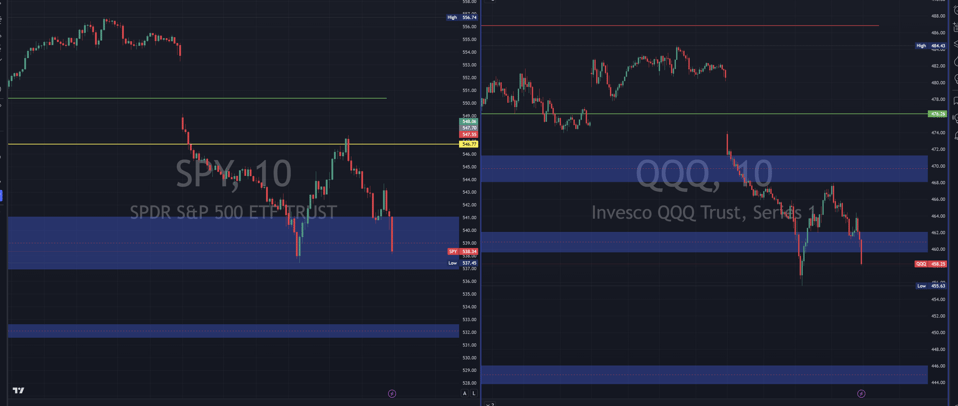

On Thursday, stock markets displayed a mixed performance, stabilizing after recent tech-led declines. The S&P 500 closed moderately lower, the Dow Jones Industrial Average added 81 points, and small-caps outperformed with over a 1% gain. The Nasdaq, however, continued its slump, finishing nearly 1% lower.

GDP Beats Expectations: A Bright Spot

The U.S. economy showed resilience, growing at a healthy 2.8% in the second quarter, surpassing the 1.9% consensus estimate. This growth, up from the previous quarter's 1.4%, was driven by robust household consumption and a notable increase in investment spending.

Key Takeaways from the GDP Report:

Consumer Resilience: Personal consumption remained strong, indicating consumers are not pulling back despite a softening labor market and slower wage growth. This continued spending should support positive economic growth for the remainder of the year.

Fed's Stance: The solid GDP growth supports the likelihood that the Federal Reserve will hold rates steady next week, with a potential rate cut in September if inflation remains moderate.

Market Volatility: A Closer Look

Recent market volatility has been fueled by disappointing earnings from tech giants like Tesla and Alphabet, leading to a rotation away from growth stocks. Despite these fluctuations, the broader market remains up, with the S&P 500 gaining over 13% year-to-date and the TSX up 5% in the past month.

Earnings Highlights:

Tech Sector: Earnings from Tesla and Alphabet disappointed, leading to a tech stock sell-off. Other tech names like Nvidia and Meta also saw declines.

Mixed Results: While companies like IBM and Chipotle exceeded expectations, Ford and American Airlines reported disappointing results, weighing on their shares.

Treasuries and Commodities:

Bond Yields: The 10-year Treasury yield fell to 4.255% from 4.285% as investors reacted to the GDP data.

Commodities: Oil prices rose 1%, while gold edged lower.

Global Perspective:

Japan: The Nikkei 225 had its worst day in over three years, falling more than 3%.

China: Despite a key rate cut aimed at bolstering growth, Chinese stocks struggled, and the yuan strengthened against the dollar.

Economic Outlook:

Consumer Spending: The GDP report highlighted an acceleration in consumer spending, a positive sign for the economy's resilience.

Inflation: Upcoming data on personal consumption expenditures (PCE) will be crucial for shaping Fed policy. Moderate inflation combined with strong GDP growth supports the "soft landing" outlook for the economy.

Conclusion:

While recent market movements have been volatile, driven by tech sector weaknesses and earnings results, the broader economic indicators remain positive. The resilience in consumer spending and better-than-expected GDP growth provide a supportive backdrop for continued, albeit moderated, economic expansion. Investors should watch upcoming economic data and Fed decisions closely as they navigate this period of adjustment and opportunity.