Market Review 21st August 2024

Simplify the craziness

DAILY REVIEW

N

5 min read

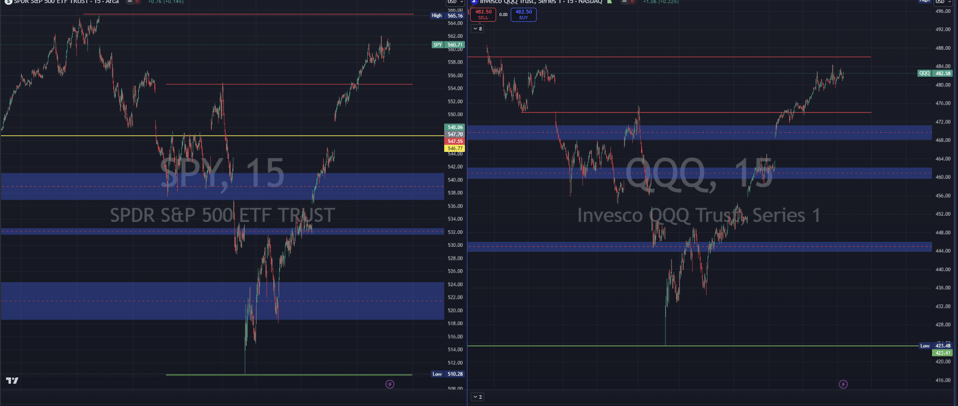

The U.S. stock markets have resumed their upward trajectory, with the S&P 500 and Nasdaq leading the way, following a brief pause in their winning streak. This resurgence is largely attributed to the latest Federal Reserve (Fed) minutes, which hint at a "likely" rate cut in September, providing a boost to investor sentiment.

Key Market Movements

S&P 500 (^GSPC): Rose around 0.4%, closing at 5,620, just shy of its all-time high.

Nasdaq Composite (^IXIC): Gained nearly 0.6%, as tech stocks continued to rally.

Dow Jones Industrial Average (^DJI): Edged up by about 0.1%, reflecting a broader market optimism.

Driving Factors Behind the Rally

The markets have been buoyed by a mix of positive corporate earnings, easing inflation concerns, and anticipation of a rate cut by the Fed in September. Here's a deeper dive into the factors propelling this market movement:

1. Federal Reserve's Minutes Signal Potential Rate Cut

The minutes from the Fed's July meeting, released earlier today, revealed that the "vast majority" of policymakers are inclined towards a rate cut in September, provided that inflation continues its downward trend. This has been a significant catalyst for the stock market's upward movement.

Inflation Trends: Recent data indicate that inflation is cooling, which strengthens the case for a rate cut. The headline Consumer Price Index (CPI) fell below 3% for the first time in over three years, signaling that inflationary pressures are easing.

Labor Market Data: New data suggests that the U.S. labor market may have been cooling earlier than initially reported. The U.S. economy employed 818,000 fewer people as of March 2024 than previously thought. While this revision indicates a softening labor market, it is not deteriorating rapidly, which may give the Fed more room to maneuver.

2. U.S. Earnings Season: A Positive Outlook

The second-quarter earnings season is nearly complete, with 95% of the S&P 500 companies having reported their results. The earnings season has been notably strong, with several key trends emerging:

Earnings Beat Expectations: Approximately 79% of companies exceeded analyst estimates by an average of 4%. The overall earnings growth for the S&P 500 was 8.3% for the quarter, slightly accelerating from the first quarter.

Sector Performance: Nine of the eleven sectors reported positive growth, with utilities, health care, and financials leading the way. Notably, the "Magnificent 7" tech stocks have continued to perform well, but earnings growth has broadened beyond these mega-cap names.

Retail Sector: Retail giants like Target, Walmart, and TJX Companies have reported strong earnings, suggesting that the U.S. consumer remains resilient despite being more price-sensitive. Target's shares surged by about 10% after the company reported better-than-expected earnings and noted an improvement in discretionary sales trends.

3. Global Market Trends

Chinese Tech Stocks Decline: On the global front, Chinese tech stocks saw broad declines after Walmart sold its stake in JD.com, raising about $3.6 billion. This sale has raised concerns about the future of Chinese tech companies, which have already been under pressure due to regulatory crackdowns.

Canadian Inflation: In Canada, inflation came in cooler than expected, which has led to a drop in government bond yields. This development has further supported the case for a potential rate cut by the Fed, as it suggests that global inflationary pressures are easing.

4. Jackson Hole Symposium: All Eyes on Powell

Investors are now turning their attention to the upcoming Jackson Hole symposium, where Fed Chair Jerome Powell is expected to deliver a highly anticipated speech on Friday. Powell's remarks will be closely watched for any signals regarding the Fed's monetary policy direction, particularly the likelihood of a rate cut in September.

Policy Normalization: Powell is likely to emphasize the need to start normalizing policy after the most aggressive tightening campaign in 40 years. With inflation moving in the right direction and the labor market showing signs of cooling, the Fed may have the flexibility to shift its focus towards maximum employment.

Rate Cut Expectations: Market expectations are high for a September rate cut, with some analysts speculating that a 0.5% reduction could be on the table. However, the Fed is expected to temper expectations of aggressive easing, as the economy remains resilient and inflation, although cooling, is still above target.

5. Market Outlook: A Bullish Trend with Potential for Volatility

While the market rally is encouraging, analysts caution that conditions could turn choppier in the near term. However, the overall uptrend is expected to remain intact, supported by strong corporate earnings and the potential for a more accommodative monetary policy.

Corporate Profits: The solid earnings growth across multiple sectors indicates that corporate profits are on firm ground, which is a key driver of the bull market. The broadening of earnings delivery beyond the mega-cap tech stocks also suggests that market gains may extend to other sectors, providing opportunities for lagging stocks to catch up.

Potential for Volatility: Despite the positive outlook, the market may experience increased volatility as investors digest the latest economic data and Fed communications. The upcoming Jackson Hole symposium will be a critical event to watch, as Powell's speech could significantly impact market sentiment.

6. Sector Highlights

Technology: The tech-heavy Nasdaq continues to outperform, driven by strong earnings from major players like Apple, Microsoft, and Nvidia. The sector's resilience has been a key factor in the broader market's recovery.

Retail: Retail stocks have been in focus, with Target leading the charge after its impressive earnings report. Walmart and TJX also provided positive outlooks, indicating that consumer spending remains robust despite economic uncertainties.

Energy: The energy sector has been relatively stable, with Exxon Mobil and Chevron posting modest gains. The outlook for oil prices remains uncertain, but the sector continues to benefit from strong demand and supply constraints.

Financials: The financial sector has seen positive earnings surprises, particularly among regional banks and insurance companies. However, the sector's performance may be impacted by the Fed's rate decisions in the coming months.

7. Conclusion: A Market in Transition

The U.S. stock market is in a period of transition, with investors weighing the potential for a rate cut against the backdrop of strong corporate earnings and a cooling labor market. While the market rally is encouraging, caution is warranted as the Fed's policy direction remains uncertain.

The upcoming Jackson Hole symposium will be a key event to watch, as it could provide further clarity on the Fed's plans for the rest of the year. In the meantime, investors should remain vigilant and be prepared for potential volatility in the weeks ahead.

References

S&P 500, Nasdaq resume climb as Fed minutes signal 'likely' September rate cut. Retrieved from MarketWatch.

Target's earnings beat expectations, shares rise 10%. Retrieved from Reuters.

Walmart sells JD.com stake, raising $3.6 billion. Retrieved from Bloomberg.

Jackson Hole symposium: What to expect from Powell's speech. Retrieved from CNBC.

U.S. earnings season: An overview of Q2 results. Retrieved from The Wall Street Journal.

Canadian inflation cools, bond yields drop. Retrieved from The Globe and Mail.

$SPY $QQQ $ES_F $NQ_F $NVDA $TSLA $AAPL $META $MSFT $AMD $AMZN $TGT $SMCI $AVGO $GOOG $LLY $SNOW $PANW $V $HD $TXN $MSTR $UNH $NFLX $COIN $MU $CRWD $TJX $XOM $ASTS $BAC $COST $ADI $PLTR $INTC $CRM $JPM $WMT $QCOM $CSCO $MA $BKNG $MRK $AMAT $MDT $C $CVX $AXP $INTU $ABBV