Market Review 1st August 2024

Simplify the craziness

DAILY REVIEW

N

4 min read

Stocks lose momentum following weak manufacturing data:

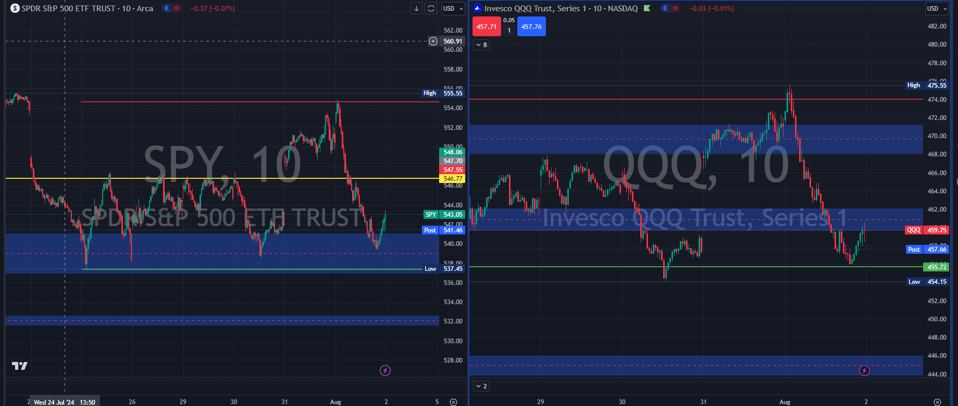

After a promising start, stocks sharply declined as a disappointing U.S. ISM Manufacturing report cast a shadow on market optimism. The manufacturing index fell to 46.8 in July, missing expectations of 48.9, marking the fourth consecutive month of contraction. This, coupled with a spike in U.S. initial jobless claims, heightened concerns over economic growth and triggered a risk-off move in the markets. Defensive sectors within the S&P 500, including consumer staples, health care, and utilities, outperformed, while growth sectors such as technology and consumer discretionary, along with U.S. small-cap stocks, underperformed.

Corporate updates:

On the corporate front, Meta's shares rose over 4% following its announcement of better-than-expected second-quarter revenue and earnings. So far, approximately 68% of companies in the S&P 500 have reported their second-quarter earnings, with 78% surpassing expectations. In the TSX, earnings will ramp up over the coming weeks, with only 37% of companies having reported their second-quarter results. Overseas, Asian markets fell overnight due to a weaker-than-expected manufacturing report from China, and European markets closed lower after the Bank of England cut its policy rate from 5.25% to 5%.

Impact on bond yields:

Weak U.S. economic data drove bond yields lower, with the 10-year GoC yield closing around 3.1% and the 10-year U.S. Treasury yield just below 4%. Market focus will remain on corporate earnings, with Amazon and Apple scheduled to report after the bell today.

Economic Data Highlights:

The week has been filled with crucial economic data releases, including U.S. labour productivity for the second quarter, initial jobless claims, and the ISM Manufacturing PMI. Nonfarm business-sector labour productivity increased by 2.3% quarter-over-quarter, surpassing expectations of 1.8% and improving from the first quarter's 0.4% increase. This productivity gain led to a rise in unit labour costs of only 0.9% in the second quarter, below the anticipated 1.7% increase. Initial jobless claims reached 249,000 last week, higher than the expected 235,000, marking the highest reading this year. Despite this increase, jobless claims remain modestly above pre-pandemic levels but below the 20-year median of over 300,000. The U.S. ISM Manufacturing PMI also fell short of expectations, indicating that higher interest rates are negatively impacting the manufacturing sector. The employment subindex dropped to its lowest level since 2020. These data points suggest a continued moderation in economic growth, inflation, and labour-market conditions, potentially paving the way for future Fed rate cuts.

July Performance Recap

Equity markets ended July on a high note, with the S&P 500 gaining just over 2%, marking its eighth monthly gain in the past nine months. The TSX also saw strong returns, climbing nearly 6% for the month, driven by robust performance from the materials and financials sectors. U.S. small-cap stocks were a standout, with the Russell 2000 Index gaining over 11%, the best monthly gain since December. The roughly 9% margin of outperformance from U.S. small-caps compared to U.S. large-cap stocks was the largest since February 2000. Overseas developed large-cap stocks and emerging-market stocks also finished higher, with the MSCI EAFE Index gaining nearly 4% and the MSCI EM Index rising over 1%. A weaker Canadian dollar in July helped boost non-domestic equity returns. In the fixed-income market, Canadian investment-grade bonds benefited from declining yields, with the Bloomberg Canada Aggregate Bond Index gaining over 2% for the month.

Most Active Stocks

Name Ticker Percentage Change (Daily)

NVIDIA Corporation NVDA -6.67%

Meta Platforms, Inc. META +4.82%

Tesla, Inc. TSLA -6.58%

Apple Inc. AAPL -1.68%

Amazon.com, Inc. AMZN -1.56%

Microsoft Corporation MSFT -0.30%

Advanced Micro Devices, Inc. AMD -8.26%

Broadcom Inc. AVGO -3.87%

QUALCOMM Incorporated QCOM -3.97%

Super Micro Computer, Inc. SMCI +4.18%

Eli Lilly and Company LLY +3.50%

Micron Technology, Inc. MU -7.57%

Intel Corporation INTC -5.50%

Alphabet Inc. GOOG -0.40%

Chevron Corporation CVX -4.89%

Boeing Company (The) BA -6.49%

Lam Research Corporation LRCX -9.87%

Bank of America Corporation BAC -2.01%

Netflix, Inc. NFLX -0.56%

JP Morgan Chase & Co. JPM -2.27%

CrowdStrike Holdings, Inc. CRWD -3.34%

Applied Materials, Inc. AMAT -7.49%

Carvana Co. CVNA +9.98%

UnitedHealth Group Incorporated UNH -0.59%

Procter & Gamble Company (The) PG +3.07%

Booking Holdings Inc. BKNG -1.37%

Goldman Sachs Group, Inc. GS -1.75%

Visa Inc. V +0.10%

Coinbase Global, Inc. COIN -5.22%

MicroStrategy Incorporated MSTR -6.36%

Exxon Mobil Corporation XOM -1.38%

Moderna, Inc. MRNA -21.01%

KLA Corporation KLAC -5.13%

Western Digital Corporation WDC -6.36%

Eaton Corporation, PLC ETN -2.27%

Merck & Company, Inc. MRK +0.61%

Texas Instruments Incorporated TXN -5.14%

Costco Wholesale Corporation COST -0.84%

Arista Networks, Inc. ANET -0.49%

Salesforce, Inc. CRM -2.22%

Home Depot, Inc. (The) HD -2.06%

McDonald's Corporation MCD +1.26%

Starbucks Corporation SBUX -3.64%

AbbVie Inc. ABBV +2.37%

PayPal Holdings, Inc. PYPL -0.71%

Caterpillar, Inc. CAT -4.24%

Pfizer, Inc. PFE +0.36%

Walmart Inc. WMT +1.68%

Mastercard Incorporated MA -0.28%

Microchip Technology Incorporated MCHP -4.97%

Analog Devices, Inc. ADI -5.39%

Johnson & Johnson JNJ +1.84%

Uber Technologies, Inc. UBER -5.35%

Citigroup, Inc. C -2.27%

Adobe Inc. ADBE -0.95%

References