Market Review 13th August 2024

Simplify the craziness

DAILY REVIEW

N

6 min read

Rally Fueled by Lower Inflation Data

Stocks and Bonds Surge on Lower-Than-Expected Inflation

On Tuesday, August 13, 2024, U.S. equity markets experienced a significant rally, bolstered by a softer-than-expected U.S. producer price index (PPI) inflation report. The positive sentiment was reflected across various sectors, with the S&P 500 gaining over 1.6% and the TSX posting a 0.9% gain. This broad-based rally was led by the information technology and consumer discretionary sectors, showcasing investor confidence in the continued growth of these areas.

S&P 500: +1.6%

TSX: +0.9%

Information Technology: Led the market rally

Consumer Discretionary: Significant gains across the sector

Global Markets Show Strength

Overseas, Asian markets also mirrored this positive momentum, with Japan's Nikkei Index seeing a substantial gain of nearly 3.5%. This rally in the Nikkei marks a strong recovery, as the index had previously declined by almost 20% in the first three trading days of August but has since rebounded by approximately 15% from its August 5 low.

Nikkei Index: +3.5%

Asian Markets: Broad gains, with Japan leading the way

Bond Yields Decline Amidst Inflation Data

The bond market also reacted positively to the lower inflation data, with yields on both U.S. and Canadian government bonds decreasing. The 10-year U.S. Treasury yield dropped to 3.85%, while the 10-year GoC yield fell to 3.03%, reflecting investor optimism about potential future rate cuts by the Federal Reserve.

10-Year U.S. Treasury Yield: 3.85%

10-Year GoC Yield: 3.03%

U.S. Inflation: Softer-Than-Expected PPI and Its Implications

The U.S. producer price index (PPI) inflation data for July came in below expectations, contributing to the day’s market rally. The headline PPI rose by only 0.1% month-over-month, below the anticipated 0.2%. Excluding volatile food and energy components, the PPI posted no change, defying expectations for a 0.2% gain.

- Headline PPI: +0.1% (expected +0.2%)

- Core PPI (excluding food & energy): No change (expected +0.2%)

Fed Rate Cut Speculation Intensifies

This softer-than-expected inflation data adds to the growing narrative of potential rate cuts by the Federal Reserve. Futures markets are currently pricing in a roughly 55% chance of a 50 basis-point (0.5%) cut at the September meeting and a total of 100 basis-points (1%) of rate cuts by the end of the year. This speculation has been fueled by consecutive months of lower-than-expected inflation readings.

Chance of 50 Basis-Point Cut in September: 55%

Total Expected Rate Cuts by Year-End: 100 Basis Points (1%)

Upcoming CPI Data and Market Implications

The focus now shifts to the consumer price index (CPI) data for July, which is set to be released tomorrow. The consensus expectation is for headline CPI to rise by 3% year-over-year, with core CPI expected to increase by 3.2% year-over-year. These figures will be crucial in shaping market expectations for future Fed actions.

Expected Headline CPI: +3% YoY

Expected Core CPI: +3.2% YoY

Retail Sales Data Anticipation

In addition to the inflation data, markets are keenly watching for key readings on consumer-spending trends. U.S. retail sales data for July, expected on Thursday, is anticipated to show a 0.3% month-over-month increase, a slight improvement from June’s no-change reading.

Expected Retail Sales Growth (July): +0.3% MoM

Earnings Reports and Consumer Sentiment

Retail earnings have also come into focus, with Home Depot reporting second-quarter earnings that exceeded expectations. Despite this, comparable sales were weaker than expected, declining by over 3%, with the company’s CEO citing higher interest rates and macroeconomic uncertainty as factors.

- Home Depot Earnings: Sales exceeded expectations, but comparable sales down by 3%

- CEO Comments: Cited higher interest rates and economic uncertainty

As the week progresses, earnings reports from major retailers like Walmart and Ross Stores will provide further insights into consumer spending trends. Overall, U.S. second-quarter personal consumption rose by 2.3%, signaling that while consumer spending may be moderating, it remains a key driver of economic growth.

- Walmart and Ross Stores Earnings: Scheduled for Thursday

- Q2 Personal Consumption Growth: +2.3%

Market Outlook: Consumer Spending Trends

In the coming months, strong household balance sheets and a healthy, albeit easing, labor market are expected to support consumer spending and extend the economic expansion, even as spending moderates from the above-trend rates seen in the second half of 2023.

Dow Jones Futures and Market Rally Analysis

Futures Movement and Market Sentiment

Following the positive inflation data, Dow Jones futures were little changed after hours, along with S&P 500 and Nasdaq futures. Investors are now turning their attention to the upcoming CPI inflation report, which is expected to further influence market sentiment.

- Dow Jones Futures: Slight decline after hours

- S&P 500 Futures: Fell by 0.1%

- Nasdaq Futures: Flat

Key Stocks in Focus

The stock market rally was led by the Nasdaq, with Nvidia (NVDA) among the standout performers. Other notable stocks that showed strong buying signals included Sea Limited (SE), Meta Platforms (META), ServiceNow (NOW), and Monolithic Power Systems (MPWR). These stocks are currently in favorable buy zones, with Nvidia’s performance being particularly noteworthy as it shrugged off competition from Huawei’s AI chip announcement.

- Nvidia (NVDA): +6.5% to 116.14, above the 21-day moving average

- Sea Limited (SE): +11.85% to 74.85, cleared a trendline entry

- Meta Platforms (META): +2.4% to 528.54, broke a trendline

- ServiceNow (NOW): +1.5% to 818.80, cleared key entry points

- Monolithic Power Systems (MPWR): +5.3% to 867.81, above the 50-day line

DOJ Considers Breaking Up Google

In a significant development, the U.S. Department of Justice is reportedly considering breaking up Google-parent Alphabet (GOOGL). This comes in the wake of last week’s antitrust victory against the internet giant. If pursued, this could lead to the separation of Google’s Android mobile operating system and Chrome web browser.

- Google (GOOGL): Fell slightly after hours; +1.15% to 164.16 during the day

- Potential Breakup: DOJ may push to end exclusive search deals and carve off Android and Chrome

Sector and ETF Performance

Various sectors and ETFs reflected the market’s optimistic sentiment. Among growth-oriented ETFs, the Innovator IBD 50 ETF (FFTY) rose by 0.4%, while the VanEck Vectors Semiconductor ETF (SMH) saw a 4.1% increase, led by Nvidia’s strong performance. On the other hand, the Energy Select SPDR ETF (XLE) fell by 1%, reflecting a broader decline in energy prices.

- Innovator IBD 50 ETF (FFTY): +0.4%

- VanEck Vectors Semiconductor ETF (SMH): +4.1%

- Energy Select SPDR ETF (XLE): -1%

Crude Oil Prices Decline

U.S. crude oil prices saw a decline of 2.1% to $78.35 per barrel, ending a five-session win streak. This drop was influenced by broader market dynamics, including the impact of the inflation report and global supply considerations.

- Crude Oil: -2.1% to $78.35 per barrel

Treasury Yields Fall

The 10-year Treasury yield fell by six basis points to 3.85%, reflecting the market’s response to the softer inflation data and anticipation of potential Fed rate cuts.

- 10-Year Treasury Yield: 3.85%

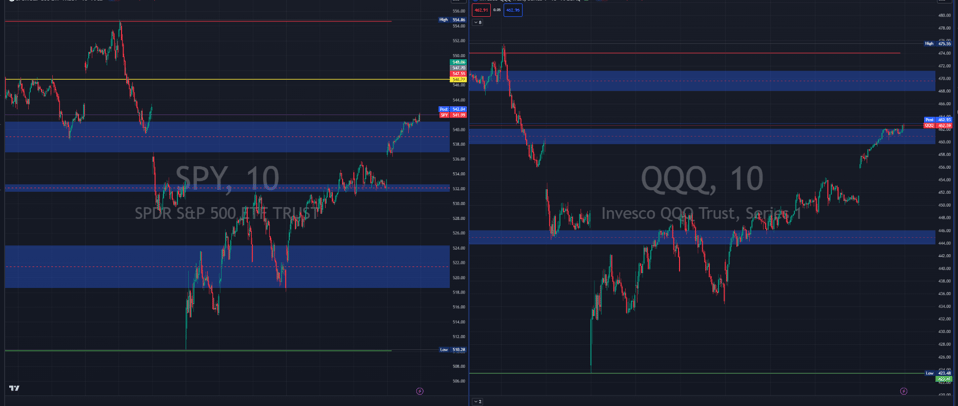

Risk-On Mindset Returns

The financial markets have rebounded dramatically since the global sell-off on August 5. With cooling inflation and a return to a risk-on mindset, particularly in the tech and growth sectors, the stock market rally appears poised to continue, though key resistance levels remain in play. The upcoming CPI report and retail sales data will serve as crucial tests for this nascent rally.

- Nasdaq and Growth Stocks: Reestablishing leadership

- S&P 500 and Nasdaq: Facing resistance at the 50-day line

Investor Takeaway

Investors should remain vigilant, looking for opportunities to add exposure as the market continues to act well. However, the outcome of key economic data, such as the CPI report, will be critical in determining the sustainability of this rally.

Table 1: Big Movers and Percentage Movements

| Stock | Ticker | Movement |

|-------|--------|----------|

| Nvidia | NVDA | +6.5% |

| Sea Limited | SE | +11.85% |

| Meta Platforms | META | +2.4% |

| ServiceNow | NOW | +1.5% |

| Monolithic Power Systems | MPWR | +5.3% |

Table 2: References

1. Inflation Report: [PPI Data Source]

2. Fed Rate Cut Speculation: [Futures Market Source]

3. Retail Sales Data: [Consumer Spending Source]

4. Earnings Reports: [Home Depot Earnings Source]

5. Bond Yield Movements: [U.S. Treasury Source]

$TSLA $SBUX $AAPL $MSFT $META $AMZN $AMD $CMG $SMCI $AVGO $LLY $V $MU $HD $GOOG $QCOM $WMT $PLTR $NKE $NFLX $ADBE $INTC $JNJ $DELL $XOM $UNH $JPM $OXY $COST $CRWD $LRCX $DIS $AMAT $PANW $CVX $UBER $MSTR $BA $MRK $CRM $PFE $TXN $BMY $CSCO $COIN $BKNG $KLAC $ADI $SHW $MA $BAC $ONON $MRVL $SHOP $HON $CVNA $TMUS $SPY $QQQ $NVDA